In April 2025, First Capital Financial Services joined the Gallagher group of companies. We are proud and excited about joining their operation to help us better serve our clients and community. Our team continues to provide specialist insurance and risk management, investment portfolio management, UK pension, and employee benefits advice for clients throughout New Zealand, and now we’re backed by global reach, expertise and partnerships.

A little bit about Gallagher

The Gallagher Group is one of the world’s leading providers of employee benefits, insurance broking, and risk management services. Its network of offices is located in over 60 countries. The parent company, Arthur J. Gallagher & Co., was founded in the United States in 1927 and is listed on the New York Stock Exchange. In Australasia, Gallagher’s Benefits & HR Consulting operation specialises in maintaining the crucial link between people’s wellbeing and organisational success through proactive people strategies that deliver results. With a commitment to confidently helping clients face the future, Gallagher combines deep local community knowledge with global expertise to provide customised advice solutions. Gallagher – Your People Strategy Partner

All Blacks Partnership

Gallagher proudly partners with organisations, events, and teams that touch communities around the globe. Locally, Gallagher becomes the Official Insurance Broker of NZR, and the brand will appear on the training and match day shorts of all NZR’s national teams, including the All Blacks, Black Ferns, Māori All Blacks, and Sevens teams. Learn more about New Zealand Rugby and Gallagher Insurance multi-year global partnership

Connect with us

For any questions about our services or our broader business, please get in touch: Please send us an email at info@firstcapital.co.nz Or give us a call on 0800 525 515

Dunedin’s Stephen Hoffman is urging people to pick up the phone and push to receive prompt treatment so their cancer does not become terminal like his did. Two brothers were both diagnosed with prostate cancer, but only one had to rely on public healthcare — and only one is dying. Dunedin resident Stephen Hoffman is a victim of the delays to cancer care in the Southern district, detailed in a damning Health and Disability Commission report released earlier this month covering the years 2016-22.

His brother Mike, who was swiftly treated for prostate cancer through the private system, believed Stephen would likely have fully recovered if not for New Zealand’s “third-world” public health care.

Stephen, 68, said time was the biggest factor in whether the cancer was treatable, and he wanted to prevent anyone else from ending up in his position. His key advice was to be proactive and call as often as it took to be sure treatment plans were progressing, as he had twice been lost in the system. “That’s what they do with people; they fob them off so that people have to go private — it’s a bit of a farce,” he said. A GP discovered his prostate issues in September 2016, but despite being classed as urgent, 10 months passed before he underwent surgery in July 2017. His biopsy took place in April of that year, and an MRI in May found almost his entire prostate replaced with a tumour. The cancer spread to his liver and lungs, and he now has a tumour at the base of his brain. Going private could have cost $40,000 and was not affordable for the former truck driver. “I couldn’t afford that, and not many people can.” Furthermore, the point of a public healthcare system was that they should not have to. Mike Hoffman, 63, said the way his brother’s case was handled was especially galling, given his family history should have made him a priority. The Christchurch resident was diagnosed with prostate cancer on Christmas Eve 2010, just weeks after a blood test showed an issue. Because of his medical insurance, he had private surgery less than three months later — including an unexpected month-long delay caused by the February 22 earthquake.

Nowadays, Employee benefits are essential to any workplace and play a significant role in attracting and retaining talented employees. Employee benefits refer to any non-wage compensation provided to employees in addition to their regular salary or an hourly wage. These benefits can take many forms, including group insurance schemes, retirement plans, paid time off, wellness programs, and other perks. Independent research conducted by Nature on behalf of Seek found that Health Insurance is the most appealing work perk a business could offer. First Capital can assist you in creating a more secure future for your staff through group insurance schemes such as group medical insurance or life, disability and serious illness cover. We can also help design and implement group retirement savings schemes to supplement KiwiSaver or provide extra benefits for Senior or Key employees. The top five perks from the survey are as follows:

Health insurance

Flexible working hours

Time in lieu

Upskilling support

Free Parking

In summary, workplace employee benefits significantly attract and retain talented employees, boost employee morale and job satisfaction, improve employee health and well-being, and enhance the employer’s reputation. A comprehensive benefits package can be valuable for employers looking to create a positive and productive work environment.

Are you planning to re-create ‘The 12 Days of Christmas’ for your true love? Brace yourself for higher costs. Just as inflation has bumped the price of food, toys and clothing, it’s impacting things like pear trees and pipers piping.

PNC’s (a US bank) Christmas Price Index notes that the overall price for the 12 gifts in the song was up 10.5% for Christmas 2022 – the third-highest increase in the 39-year history of the calculations.

You would have spent $45,523.27 last Christmas if you had picked up each of the 12 items mentioned. If you’re a stickler for detail and bought everything in the song (saddling your poor paramour with 12 pear trees and more birds than many aviary sanctuaries), you’re looking at a bill of $197,071 – and high odds that you’ll either be dumped by New Year’s Eve or viciously attacked by those 42 jerk geese you thought were a good gift idea.

It’s the five gold rings that saw the most significant increase last Christmas. The price of those jumped more than 39% as commodity prices spiked. Turtle doves were close behind, with a 33.3% price increase over last year. Higher fertilizer costs mean you’ll pay an extra 25.8% for the partridge in a pear tree (that bird, actually, costs the same as Christmas 2021 —as do the swans-a-swimming).

There’s definitely a glass ceiling in this song, as the lords-a-leaping saw their value increase 24.2% (and they’re, by dollar value, the most expensive item on this year’s index, coming in at $13,980). Ladies dancing, though, saw just a 10% jump to $8,308.

And let’s not even talk about the injustices for maids-a-milking, who haven’t seen a pay raise since 2009. The line-item cost for those hard-working women? Just $58.

How much have things changed through the years? Shoppers who purchased all 12 items back in 1984 would have paid less than half of today’s cost, shelling out just $20,069.58. And the index hit an all-time low in 1995 when it dropped to $17,915.25.

Still, think inundating your love with fowl and service people is the way to go? (Does your true love even HAVE a cow, much less eight that need to be milked??) Here’s how the gift prices break down:

More companies are looking to enhance their benefit offering this year, despite cost constraints, according to new research. Gallagher found eight out of 10 employers who are planning changes to their benefits package are looking to enhance their benefits package This is an increase from the 70 per cent looking to upgrade services last year.

Of those planning changes, only 5.2 per cent are looking to remove benefits, which the consultant says shows the value of a clear benefits strategy, particularly when it comes to recruitment and retention in a difficult employment market.

The research also showed that 23.5 per cent of firms are going to change their benefit delivery method, with the same percentage looking to switch their benefits provider.

The research, part of Gallagher’s fifth benefit strategy and benchmarking survey report, looked at the challenges facing businesses when it comes to delivering a successful benefits strategy. The research found the biggest challenge cited by businesses was to ensure their benefits offering appealed to a diverse workforce that will have very different needs and preferences.

Other major concerns included increasing the cost of benefits within a tight budget and challenges around the communication of benefit packages.

Last year costs and budget were seen as the biggest challenge, so this is the first time the issues around diversity have now superseded this to become the number one concern.

The research revealed that the majority of employers haven’t implemented policies needed to support women in the workplace experiencing menopause – with only one in five firms with formal policies in place. Where support for women during menopause exists, the type of help being offered ranges from flexible working policies (61.5 per cent), employee forums/support groups (53.8 per cent) and training for managers (42.3 per cent).

Gallagher’s data shows 73 per cent of organisations are looking to improve internal communication – but as many as two-thirds (68.6 per cent) do not have a pre-defined benefits communication budget. Among those surveyed with a communication budget, most allocated less than £10,000 per year. The use of a discount portal is one of the top (33.9 per cent) methods used to communicate, followed by 17 per cent using mental health/well-being apps.

Steve Threader, managing director of reward and benefit consulting at Gallagher’s Benefits and HR Consulting Division in the UK, says: “The connection between employee wellbeing and organisational wellbeing has become more significant. It’s encouraging to see that the desire to create flexibility is trending across the country, with 47.8 per cent of employers wanting to improve it in order to extend individual choice and to better support those who need it the most.”

Our global population is getting older. By 2050, the OECD predicts that 30% of people worldwide will be aged 65 or over.

While some countries are relatively prepared to handle this increase in the elderly demographic, others are already feeling the squeeze and struggling with the challenges that come with a rapidly aging population.

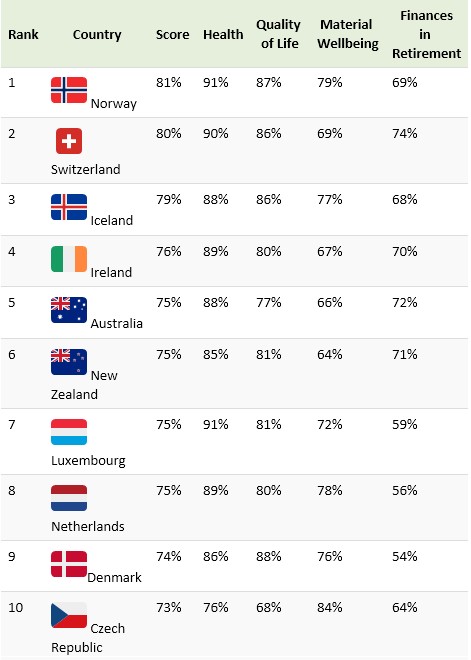

Which countries are the best equipped to support their senior citizens? This graphic uses data from the 2022 Natixis Global Retirement Index to show the best countries to retire in around the world based on several different factors that we’ll dig into below.

What Makes a Country Retirement-Friendly? When people consider what makes a place an ideal retirement location, it’s natural to think about white sand beaches, hot climates, and endless sunny days. And in truth, the right net worth opens up a world of opportunities to enjoy one’s golden years.

The Global Retirement Index (GRI) examines retirement from different, more quantitative perspective. The annual report looks at 44 different countries and ranks them based on their retirement security. The index considers 18 factors, which are grouped into four overarching categories:

Health: Health spend per capita, life expectancy, and non-insured health spend.

Quality of Life: Happiness levels, water and sanitation, air quality, other environmental factors, and biodiversity/habitat.

Material Wellbeing: Income per capita, income equality, and employment levels.

Using these 18 metrics, a score from 0.01 to 1 is determined for each country, which is then converted to a percentage. For a more detailed explanation of the report’s methodology, explore Appendix A (page 72) of the report.

The Top 25 Best Countries to Retire in With an overall score of 81%, Norway ranks number one as the most retirement-friendly country on the list.

Norway is at the top of this year’s ranking for several reasons. For starters, it achieved the highest score in the Health category, mainly because of its high average life expectancy, which is 83 years old, or nine years longer than the global average. Norway also has the highest score of all the countries for Governance, a category gauged by assessing country corruption levels, political stability, and government effectiveness, and is in a three-way tie with Japan and Luxembourg in the Health category. Second on the list is another European country, Switzerland, with an overall score of 80%. It’s the highest-ranked country for environmental factors and has the highest overall score in the Finances in Retirement category.

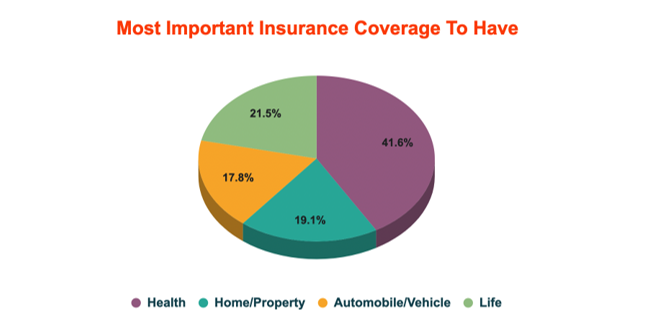

An international survey found that a more significant percentage of people feel that life insurance is more important than home/property or vehicle insurance.

The survey of 1,000 people spanning the US, UK, Canada, and parts of continental Europe, undertaken by international software vendor Zelros, canvassed what type of insurance people felt was essential.

Zelros says while the majority of people, at 41.6%, say “health insurance”, the most common answer at 21.5% was life insurance, followed by home/property insurance at 19.1%. The least common response, with 17.8%, was automobile/vehicle insurance.

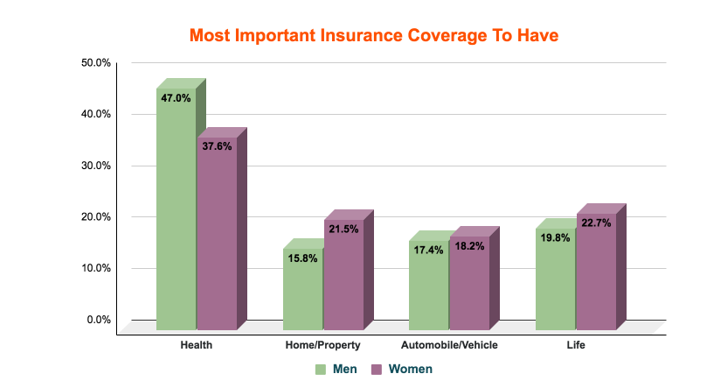

Zelros, which develops AI systems for insurance and bank insurance players, notes that 47% of men surveyed feel the most important insurance coverage is health, followed by 19.8% who think that life insurance is most important. Another 17.4% feel automobile/vehicle insurance is the most important, and 15.8% believe home insurance is the most important.

Of the women surveyed, 37.6% consider health insurance most important, while 22.7% believe life insurance is most important, followed by home insurance at 21.5%. Automobile/vehicle insurance came in last for women at 18.2%.

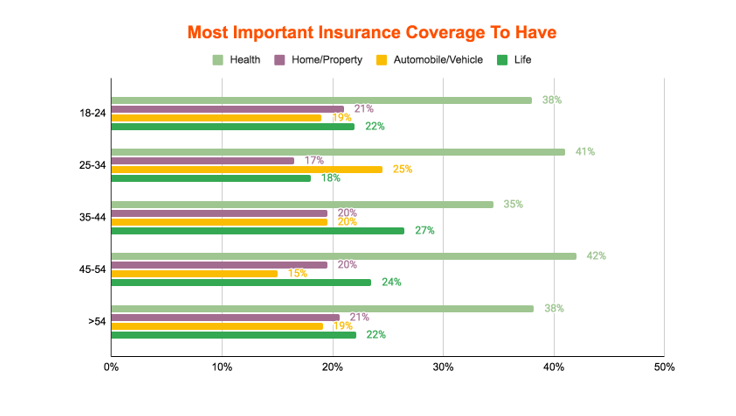

While health was again the most important type of insurance to have across all age groups, 22% of 18-24 year-olds opted for life insurance; as did 18% of 25-34 year-olds; 27% of 35-44 year-olds; 24% of 45-54 year-olds and 22% of >54 year-olds.

Disclaimer: This article only provides general information; it does not consider your personal needs or circumstances and is not intended to be viewed as financial advice. If you require financial advice, contact one of our financial advisers.

Stock markets rose again on Friday, capping off July’s massive rebound, which has brought relief to investors following the worst start to a year in over five decades. The S&P500 rose 1% on Friday for a 9.1% rise last month, the biggest monthly gain since November 2020. It was the best July for the broader index since 1939.

The tech-laden Nasdaq did even better with a gain of 12% in July, the strongest monthly gain since April 2020. Strong earnings from tech titans Amazon and Apple boosted sentiment on Friday. Amazon shares rallied 10% and finished up a somewhat incredible 27% in July (although they are still down 20% year to date).

The market’s incredible performance in July has the hallmarks of a reset by investors after a lot of bad news had been priced in. Concerns around inflation, interest rates and the economy remain, but the worst-case outcomes have yet to play out, and the future may also not be as bad as feared. Inflation could be peaking while softening patches in the economy have seen the Federal Reserve pivot to a more dovish stance.

The world’s largest economy contracted for the second quarter in a row, but to paraphrase Star Trek, “it’s a recession but not as we know it, Jim.” An obvious difference from a usual recession is a strong jobs market and an economy which created nearly 400,000 jobs last month. Consumers, while being more ‘choosy,’ are also still outspending on a variety of products and services, as highlighted by the current US earnings season.

On that note, the reporting season continues to deliver many more positives than negatives. Over 70% of S&P500 companies that have reported to date have beaten earnings expectations.

On Friday, Amazon beat quarterly revenue and earnings forecasts and gave an upbeat outlook for the rest of the year. Revenues rose 7% to US$121b, with the cloud computing business doing particularly well. Amazon was a massive pandemic beneficiary, but post the peak consumer spending boom; the company was left with excess warehousing and overstaffing. Investors were buoyed that the company is cutting back on costs, even while overall revenues are still inching higher. Amazon made a loss during the quarter (mainly due to an investment in EV maker Rivian) but expects operating income to be as much as US$3.5 billion in the current quarter.

There was a similarly upbeat update from Apple. The company saw revenues rise 2% to US$83 billion during the quarter, nearly half of which was iPhone sales. The company had warned that supply chain constraints would have a US$4 to $US$8 billion impact during the quarter, and in the end, it was less than US$4 billion. This was music to the ears of investors. On that note, Apple Music saw sales surge 12% to US$19.6 billion. Apple is also cutting costs, but customers are out there spending strongly on the company’s products and services, further contradicting the idea that we are in recession.

There continue to be some earnings misses to temper enthusiasm from getting overblown. Intel shares fell 8.6% after the company reported quarterly revenue of US$15.3 billion, which was well short of the US$17.9 billion expected. Earnings per share of 29 cents were well short of the 70 cents expected. It was the company’s largest top-line disappointment since 1999, with the semiconductor maker wearing the impacts of slower computer purchasing by corporates. The company lowered full-year guidance but provided a ray of light, with executives saying the chip-maker was “on the bottom.” The only way may be up, with Intel also putting through price increases.

The European economy is already off the bottom, it seems. Preliminary figures from Eurostat showed GDP grew 0.7% quarter on quarter in June when a tepid gain of 0.1% had been expected. While Germany lagged, Spain and Italy saw growth of 1%, while the French economy grew in the quarter when a contraction had been expected. An influx of tourists post lockdowns has also provided a boost to the Eurozone.

The Euro economy is dealing with challenges still (inflation has hit 8.9%), but like many places, a lot of bad news has been priced in. The Stoxx50 in Europe also had a strong month, rallying 7.6%. The FTSE100 in the UK added nearly 7% in July. Shares in UK bank Natwest surged 8% after earnings beat expectations, with higher rates boosting earnings while credit provisions were reduced. The Bank of England meets Thursday with a 50bps rate rise on the cards.

L’Oreal shares rose after reporting strong sales and plans to continue putting through price rises to offset higher production costs. Luxury good makers Hermes jumped 7% after reporting record earnings. Growth in the US was strong while China rebounded. The maker of Birkin bags (custom-made ones can go for US$100,000+) has maintained ambitious growth targets. What recession?

Disclaimer: This article only provides general information; it does not consider your personal needs or circumstances and is not intended to be viewed as financial advice. If you require financial advice, contact one of our financial advisers.

“Regular saving makes you love – and long for – bear markets.”

Nick Murray

They say “consistency is more powerful than perfection”, which also applies to growing your investment portfolio! One way to manage investment risk during a volatile market is to save regularly, called “dollar-cost averaging”. KiwiSaver is an excellent example of “dollar-cost averaging”. The idea is to invest a set amount of money at regular intervals no matter how the stock market performs. With this approach, you will be able to buy more shares when prices are lower and fewer shares when prices are higher. As a long-term investor, you should be less concerned about the current price of stocks and more interested in the number of shares you can accumulate over time. You want to accumulate the largest quantity of shares possible. Adding a consistent dollar amount to your investment account regularly to buy as many shares as possible and buying more when prices are lower will help you achieve that goal. You cannot control share prices and cannot predict with consistent accuracy when prices will change. You can control how much you invest and the strategy you implement. Focus on accumulating as many shares as you possibly can. The best way is to keep saving consistently over time. Click on the link to learn more about the Power of Regular Savings, including a Hypothetical Scenario, by Ben Brinkerhoff from Consilium.

Disclaimer: This article is intended to provide general information only. It does not take into account your personal needs or circumstances and is not intended to be viewed as investment or financial advice. Should you require financial advice, you should contact one of our financial advisers—past performance is not a guarantee of future performance.

‘Just as many people were starting to think markets only ever move in one direction, the pendulum has swung the other way.’

Jim Parker of Dimensional Fund Advisers

Volatility is back. Just as many people were starting to think markets only ever move in one direction, the pendulum has swung the other way. Anxiety is a completely natural response to these events. Acting on those emotions, though, can end up doing us more harm than good.

There are a number of tidy-sounding theories about why markets have become more volatile. Among the issues frequently splashed across newspaper front pages: global growth fears, policy uncertainty, geopolitical risk, and even the Ebola virus.

In many cases, these issues are not new. The US Federal Reserve gave notice last year it was contemplating its exit from quantitative easing (an unconventional monetary policy used by central banks to stimulate the economy when standard monetary policy has become ineffective). Much of Europe has been struggling with sluggish growth or recession for years, and there are always geopolitical tensions somewhere.

In some ways, the increase in volatility in recent weeks could be just as much a reflection of the fact that volatility has been very low for some time. Investors in aggregate were satisfied earlier this year with a low price on risk, but now they are applying a higher discount rate to risky assets.

So the increase in market volatility is an expression of uncertainty. Markets do not move in one direction. If they did, there would be no return from investing in stocks and bonds. And if volatility remained low forever, there would probably be more reason to worry.

As to what happens next, no one knows for sure. That is the nature of risk. In the meantime, investors can help manage their risk by diversifying broadly across and within asset classes. We have seen the benefit of that in recent weeks as bonds have rallied strongly.

For those still anxious, here are seven simple truths to help you live with volatility:

Don’t make presumptions.

Remember that markets are unpredictable and do not always react the way the experts predict they will. When central banks relaxed monetary policy during the crisis of 2008-09, many analysts warned of an inflation breakout. If anything, the reverse has been the case with central banks fretting about deflation.

Someone is buying.

Quitting the equity market when prices are falling is like running away from a sale. While prices have been discounted to reflect higher risk, that’s another way of saying expected returns are higher. And while the media headlines proclaim that “investors are dumping stocks,” remember someone is buying them. Those people are often the long-term investors.

Market timing is hard.

Recoveries can come just as quickly and just as violently as the prior correction. For instance, in March 2009—when market sentiment was at its worst—the S&P 500 turned and put in seven consecutive months of gains totalling almost 80%. This is not to predict that a similarly vertically shaped recovery is in the cards, but it is a reminder of the dangers for long-term investors of turning paper losses into real ones and paying for the risk without waiting around for the recovery.

Never forget the power of diversification.

While equity markets have turned rocky again, highly rated government bonds have flourished. This helps limit the damage to balanced fund investors. So diversification spreads risk and can lessen the bumps in the road.

Markets and economies are different things.

The world economy is forever changing, and new forces are replacing old ones. This applies both between and within economies. For instance, falling oil prices can be bad for the energy sector but good for consumers. New economic forces are emerging as global measures of poverty, education, and health improve. A recent OECD study shows how far the world has come in the past 200 years.

Nothing lasts forever.

Just as smart investors temper their enthusiasm in booms, they keep a reserve of optimism during busts. And just as loading up on risk when prices are high can leave you exposed to a correction, dumping risk altogether when prices are low means you can miss the turn when it comes. As always in life, moderation is a good policy.

Discipline is rewarded.

The market volatility is worrisome, no doubt. The feelings being generated are completely understandable and familiar to those who have seen this before. But through discipline, diversification, and understanding how markets work, the ride can be made bearable. At some point, value re-emerges, risk appetites reawaken, and for those who acknowledged their emotions without acting on them, relief replaces anxiety.

Source: Jim Parker, from the book, “Outside the Flags”.

This article was written on October 28th, 2014. We feel the points addressed almost ten years ago are once again relevant in today’s market.